“I read the policy documents. But I still can’t figure out what any of it means for my workshop.” At Kogei Japonica, we hear this often — in interviews, consultations, and conversations with people working in the field. Policy documents from Japan’s Ministry of Economy, Trade and Industry (METI) carry a lot of information, and they tend to be read primarily as guides to available subsidies. But the 2026 policy discussions contain something more substantive — changes that connect directly to how craft workshops run their businesses.

The document worth paying close attention to is the materials from the 12th session of METI’s Entertainment and Creative Industries Policy Study Group, published on February 4, 2026. In it, Japan’s government-designated traditional craft industries are explicitly named as part of the creative industries framework, and the document sets out a clear direction: to link regional economic development with the growing demand for Japanese craft in overseas markets, and to examine how cross-sector collaboration can strengthen that reach.

This article uses the 12th session materials, the broader policy context as of March 2026, and the structure of the Traditional Craft Industries Promotion Act as its starting points. From there, it works through what kogei businesses, regional governments, corporate buyers, and support organizations should be focusing on — from a practical business perspective.

Reading policy is not the same as scanning for subsidy opportunities. It means understanding what is being prioritized at a structural level, and using that to calibrate your own decisions. That is the purpose of this article.

Table of Contents

How Kogei Businesses Should Read METI’s 2026 Policy

The short version: the 2026 policy discussions signal a growing emphasis on demand creation, domestic and overseas sales channels, and cross-sector collaboration. This is not a retreat from supporting traditional craft — it reflects a recognition that for the sector to survive as an industry, it needs functioning revenue structures: real demand, accessible distribution, and economics that can sustain makers over time.

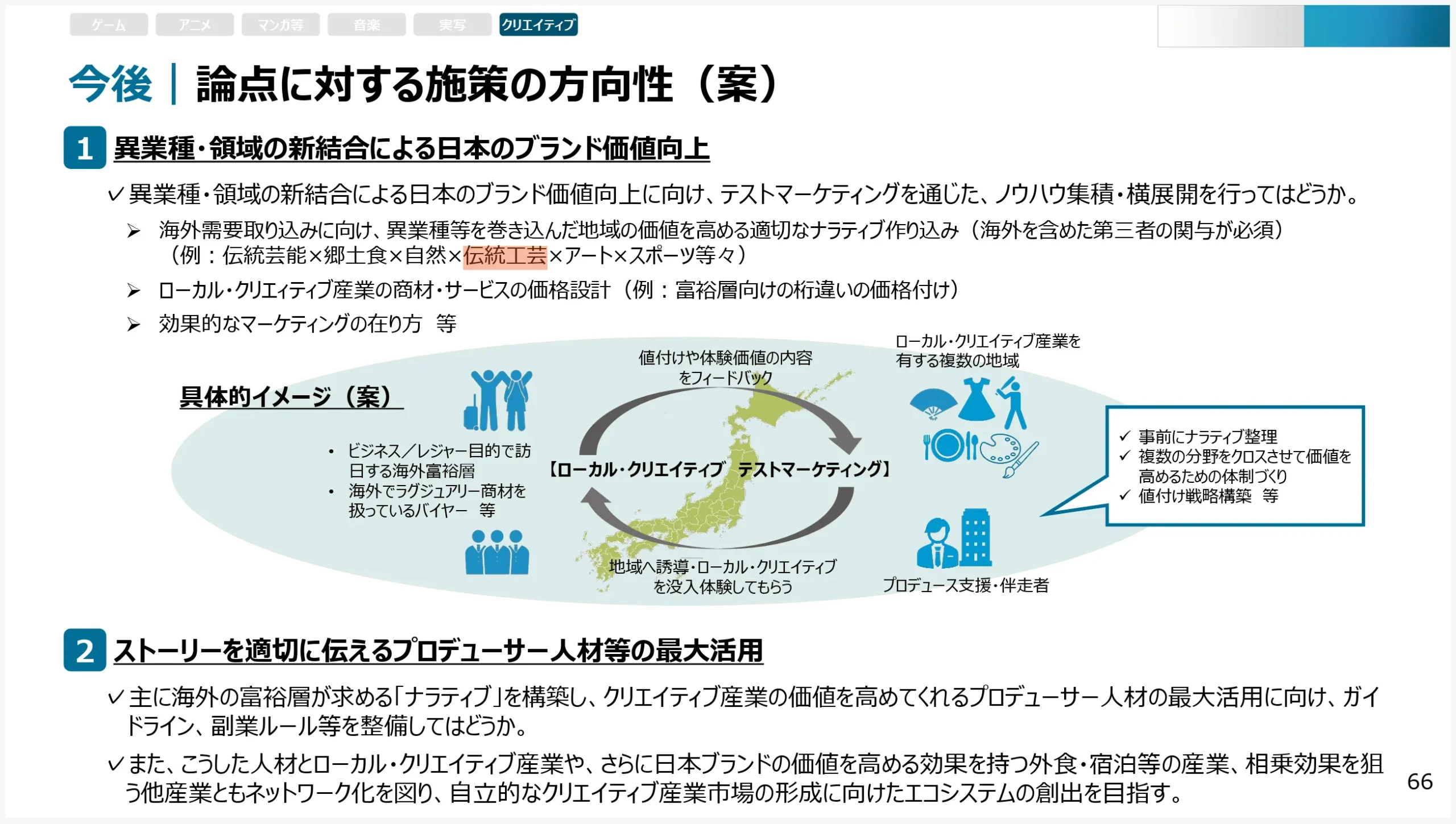

What the February–March 2026 Policy Discussions Made Clearer

The 12th session materials from METI’s Entertainment and Creative Industries Policy Study Group, published on February 4, 2026, explicitly named Japan’s government-designated traditional craft industries as part of the creative industries framework. The document also set out the direction that, on the premise of contributing to regional economic vitality, measures to increase the appeal of Japanese creative industries to growing overseas demand — through cross-sector collaboration — would be examined.

(Source: 12th Session: Entertainment and Creative Industries Policy Study Group (Secretariat Materials) | METI)

The same document raised “the development of high-value local creative industries” as a key agenda item. The framing positions regionally rooted industries — including traditional craft — as growth sectors with significant latent demand, particularly among global luxury consumers, but ones that have not yet been able to fully realize that value or build viable business models around it. Traditional craft sits at the center of that reframing.

METI’s FY2026 budget request also outlined the direction of support for traditional craft industries as “supporting the development of appealing new products and the expansion of domestic and overseas sales channels.”

(Source: FY2026 Expenditure Budget Request | METI)

What matters here is that “development” and “sales channels” are placed side by side. The policy is putting meaningful weight on the question of where things go once they are made — who buys them, and through what structure.

Why Reading Policy Only as Subsidy Information Leads Nowhere

Subsidies are useful tools. But consuming policy documents only for subsidy leads does not produce real strategy.

The failure pattern is consistent. A workshop uses an exhibition subsidy to attend an overseas trade fair. Business cards are exchanged. Then nothing moves. The show itself became the goal, and the question of how to build a continuing sales relationship afterward was never seriously addressed.

Reading policy means reading what is being set as the evaluation criteria. In the current policy context, what is being valued is not one-off activity but sustained channels, ongoing partnerships, and measurable outcomes. Knowing that is what allows you to design your own actions accordingly.

The Five Practical Themes This Article Covers

The sections that follow work through five interconnected themes: overseas sales, channel design, artisan succession, cross-industry collaboration, and an action checklist you can use immediately. These are not separate topics — they are connected by a single thread: building a revenue structure that works.

International Growth Starts with Channel Design, Not Export Alone

Getting into an overseas market and continuing to sell in one are entirely different challenges. Most conversations about international sales focus on the first and defer the second. This section approaches the question from the other direction: who are you selling to, what are you offering, and how do you build a structure that keeps working?

Why Japanese Craft Is Being Reassessed in Overseas Markets Right Now

The 12th session materials noted that, within the creative industries, concrete targets should be considered in anticipation of expanding overseas demand going forward. They also identified the promotion of local creative industries — those with significant latent demand, particularly from global luxury consumers, that have not yet been able to develop high-value offerings or build commercial models around them — as a key policy challenge.

The point is not simply that Japanese craft has international appeal. The real work lies in the specifics: how to position a product as a high-value offering, for which market, with what narrative, and at what price point. That is the design problem.

Part of what gives Japanese craft traction in overseas markets is that its value is not easily replicated elsewhere — the cultural context, the production philosophy, the story of a specific region all contribute something that quality alone cannot. Whether that context is being communicated in English, in a form that buyers can actually use, is often where the difference lies between recognition and revenue.

How to Make Practical Use of TAKUMI NEXT and JETRO Support

TAKUMI NEXT is a Japan External Trade Organization (JETRO) program designed to help Japanese craft and maker businesses expand into overseas markets. It includes facilitated online business meetings, support for overseas-facing social media communication, and matching with international buyers.

(Source: TAKUMI NEXT 2026 | JETRO)

The critical point is not to treat acceptance into the program as the goal. Getting practical value out of it requires thinking through each stage separately.

- Application and acceptance: You need a clear target buyer in mind, and English-language product descriptions as a baseline.

- Business meetings: Conversations cannot move forward without the ability to clearly state sample availability, pricing terms, minimum order quantities (MOQ), and lead times.

- Follow-up: An English follow-up within two weeks of a meeting is often what determines whether the conversation continues.

- Ongoing orders: Repeat business requires building credibility over time — giving buyers reasons to come back.

There is a difference between using a program and getting something out of it. JETRO’s programs are entry points. How well a workshop is prepared for what comes after will determine whether anything actually moves.

Cross-Border E-Commerce Is a Supporting Channel, Not the Core Strategy

Cross-border e-commerce receives a lot of attention as an overseas sales route for traditional craft. In practice, however, operating an e-commerce channel before establishing name recognition tends to produce limited results in this sector.

The reason is structural: e-commerce reaches people who already know who you are. Reaching overseas buyers and consumers who have never encountered your work requires something that builds awareness first — trade shows, media coverage, social media, direct B2B outreach. Those come before the sale.

Cross-border e-commerce works best as a destination for buyers who have already encountered the work through another channel. It should be designed as a follow-through mechanism, not a starting point.

Common Failure Points and How to Address Them

Most international sales problems have less to do with product quality and more to do with the supporting materials not being in place. Four patterns come up consistently.

- No English-language materials: Product names, descriptions, and the maker’s story exist only in Japanese, leaving nothing to hand a buyer. The fix is straightforward: prepare a one-page English product sheet before you need it.

- No price list: Being asked “price list please” at a trade show and having nothing to hand over stops the conversation immediately. A document with wholesale prices, suggested retail prices, and MOQ is non-negotiable.

- No use-case proposals: When a buyer asks what this is for, or where it goes, the answer needs to be ready. Photographs showing the piece in a real context — a hotel room, a restaurant table, a residential interior — are more persuasive than any description.

- No follow-up after meetings: If there is no follow-up email within one to two weeks of a trade show meeting, buyers move on to other suppliers. Sending a brief thank-you with materials attached — ideally the same day or the next — is the habit that keeps conversations alive.

For Stable Revenue, B2B Channel Design Matters More Than Direct-to-Consumer Sales

Direct-to-consumer sales matter, but the more reliable path to sustainable revenue for traditional craft businesses runs through B2B — selling to organizations rather than individuals. The unit values are higher, the orders are larger, and the relationships tend to continue. With sales channel development as a stated policy priority, this is where makers should be concentrating their effort.

Three Channel Priorities for Domestic and International Sales Development

When you organize the options, three channels stand out as the most worth pursuing.

- Corporate procurement: Hotels, restaurants, offices, healthcare facilities — organizations that incorporate craft into their spaces tend to place high-value orders and maintain long-term relationships. Architectural firms and interior designers are often the most productive entry point.

- Gallery and curated retail: Department stores and select shops involve challenging wholesale negotiations, but they serve an important function in building brand recognition. The goal in these channels is not only to sell but to be seen.

- Inbound tourism touchpoints: Craft retail at tourist destinations, experience facilities, and airport shops reaches international visitors before they encounter overseas channels. These spaces function as awareness-builders that support later B2B conversations and e-commerce.

What the 12th Session Materials Mean for High-Value Positioning and Sales Design

The 12th session materials outlined three orientations for developing local creative industries: identifying and developing high-value products and services, maintaining that value while opening sales channels, and generating purchase intent.

For many workshops, the question is not whether the work has value. It is how that value can be carried into markets without flattening the skill, culture, and relationships behind it. Making something well is not sufficient on its own. You need to define who finds it high-value, choose distribution channels that protect that positioning, and design the narrative and presentation that actually motivates someone to buy. All three are part of the job.

Sales channel development, in this reading, is not simply adding more outlets. It means selecting channels that protect your pricing, communicate the work’s context, and generate the kind of ongoing relationships that produce repeat business.

The Most Common Mistake in Publicly Funded Sales Support

From a support-provider perspective, the most frequent failure is “hold an event, done” or “issue a press release, done.” Neither is useless, but neither should be the end product of a support program.

The core question is whether a buyer has been identified and a path to a sale has been designed. Who is going to purchase this work? Which organizations might adopt it, and for what purpose? How will that relationship be maintained? These questions need to be answered at the program design stage, not after the event has happened. That requires support organizations to come in with both the commitment to stay involved and the knowledge of how sales channels actually work.

The Minimum Sales Materials Every Workshop Should Have

Opening sales channels requires more than product — it requires the materials to communicate it. At a minimum, the following should be in place.

- An English-language product description (one A4 page is enough to start)

- A price list with wholesale prices, suggested retail prices, and MOQ

- Standard lead time information

- Photographs showing the piece in use within a real space

- Example applications for corporate buyers

The number of makers who put this off is significant. It does not need to be perfect. It needs to exist.

The Artisan Succession Problem Is About Revenue Structure, Not Recruitment

Conversations about succession in craft often focus on the absence of young people willing to enter the field, or the lack of someone to take over a workshop. But the interest is there — what is harder to find is a plausible income trajectory. The underlying problem is structural.

Succession is not primarily a recruitment or awareness problem. It is a revenue structure problem. Addressing it without addressing the economics is unlikely to produce lasting results.

Under the Legislation, Demand Development and Succession Are the Same Problem

The Traditional Craft Industries Promotion Act lists both the development of the industry and the securing of the people who carry it forward as its core purposes.

(Source: Act for the Promotion of Traditional Craft Industries | e-Gov Law Database)

The Act’s implementing regulations also explicitly include “sales development, joint sales, and information provision” as components of joint promotion plans.

(Source: Implementing Regulations of the Act for the Promotion of Traditional Craft Industries | e-Gov Law Database)

The implication is built into the legislation: creating markets and securing makers are treated as a single challenge, not separate ones. When sales channels expand, workloads increase. When volumes and unit prices rise, the work becomes something worth committing to. Succession policy needs to be designed with this structure in mind.

What Production Districts That Retain Young Makers Have in Common

Across our reporting in production districts around Japan, a consistent set of conditions appears in places where young makers stay.

- Work volume is reasonably stable

- Unit prices are gradually increasing

- There is external recognition — through media, awards, or overseas demand

- There are connections to urban markets or other industries

- A division of labor exists, so no single person has to carry every function

That last point tends to be underweighted. A workshop where one person handles everything — making, selling, communicating, administering — has limited capacity to scale or improve its economics. Districts with some division of labor between production, sales, communications, and management tend to be healthier over the long term.

Bringing in Specialists on a Part-Time or Project Basis Is a Practical Option

For districts and workshops where full-time hiring is not feasible, bringing in freelance or part-time specialists is a workable approach. Designers, sales support, translators, social media managers, marketers — functions outside of production can be supplemented externally, which allows makers to concentrate on the work itself.

This should not be seen as a compromise. It can be a deliberate structural choice: defining roles clearly and building the workshop’s capabilities intentionally. In districts that already have connections to urban professionals, this kind of arrangement is increasingly viable and worth watching as a model.

A Common Misconception

The idea that expanding hands-on workshops will produce more makers is repeated often, but the connection is weak in practice. Workshops are a point of entry into awareness, not a pipeline into the profession. People do move from workshops into craft careers, but whether they do depends far less on the number of sessions run and far more on what comes after — the structure of ongoing contact and, critically, the visible economic case for making it a livelihood.

Cross-Industry Collaboration Should Generate Work, Not Just Publicity

Collaborations and partnerships have become a familiar part of craft industry conversation. So has the pattern of a well-photographed launch that leads nowhere. The question to ask about any collaboration is not whether it generated attention but whether it produced ongoing revenue or work.

Which Partner Categories Tend to Work Well

Looking at sector characteristics, some categories stand out.

- Architecture and interiors: There is real demand for integrating craft materials and techniques into spaces. When makers can be involved at the design stage, unit values are high and project-based orders tend to recur.

- Hotels and hospitality: Guestrooms, lobbies, tableware, and amenities are all areas where craft adoption is under active consideration. Organizations in this sector have clear brand motivations, which makes the business case easier to establish.

- Apparel and fashion: Brands looking to differentiate through materials, patterns, or techniques exist and are worth pursuing. The trade-off is that this sector is more sensitive to trend cycles, which creates variability in how long collaborations continue.

- Content and place branding: There is genuine appetite for craft as narrative — in tourism, relocation promotion, and regional identity work. These partnerships often involve an exchange of reach rather than direct payment, so managing expectations carefully matters.

What the 12th Session Materials Mean for Cross-Sector Partnership in Practice

One thing worth noting about the 12th session materials is that cross-sector collaboration is not treated as a PR mechanism. The document addresses local creative industries in concrete terms: clarifying the narrative in advance, building structures that combine multiple fields to increase value, developing pricing strategy, and running test marketing. These are operational considerations, not communications ones.

(Source: 12th Session: Entertainment and Creative Industries Policy Study Group (Secretariat Materials) | METI)

Rather than selling craft in isolation, the question is how to combine it with food, hospitality, art, content, or spatial design in ways that shift the price point, the experience, and the market reached. The combination changes what is possible.

What Separates Collaborations That Work from Those That Don’t

Collaborations that produce real outcomes are generally designed so that both parties have something concrete to gain, and both parties know what that is. Does the partnership solve a problem for the other organization? Does it produce measurable improvement in revenue or positioning for the craft side? If those questions were not addressed in the design phase, the likely result is a set of good photographs and nothing further.

Common failure modes: one side holds disproportionate control, success is measured only in coverage, and there is no planned next step after the initial project concludes.

How to Avoid the Single-Year Trap in Government-Supported Projects

Government-supported collaboration projects are structurally predisposed to ending after one year, because they are tied to annual budget cycles. This is a genuine constraint.

The way around it is to build the continuation into the design from the start — specifying, as a deliverable, what relationships and structures should be in place to continue without public funding after the project ends. Whether a collaboration outlasts a subsidy cycle is usually decided at the design stage, not afterward. Regional bodies and support program managers who engage with these projects should treat that as a design requirement, not an afterthought.

Actions Makers, Regional Bodies, and Corporate Teams Should Take Now

The sections above have covered policy context, international sales, channel design, succession, and cross-sector collaboration. This final section organizes the practical takeaways by role — at the level of what can be done this week.

For Kogei Businesses and Makers

- Do you have a one-page English product description ready to hand over?

- Do you have a price list with wholesale prices, suggested retail prices, and MOQ?

- Do you have use-case proposals with photographs for corporate buyers?

- Do you know your unit prices and gross margins, and do you have a revenue target?

- Do you have at least one active contact with a potential collaboration partner — a designer, trading company, or architectural firm?

Related Articles

For Regional Bodies and Support Organizations

- Is there a follow-through support structure in place after makers are accepted into a program?

- Are your outcome measures anything other than number of appearances or media mentions?

- Have you designed a process for matching workshops with actual buyers or adopting organizations?

- Is there a mechanism for self-sustaining activity built into the program design for after support ends?

For Corporate and Business Development Teams

- Is craft being treated as a brand asset rather than a procurement cost?

- Is there a plan for ongoing orders and relationship-building with the makers and districts you work with?

- Do you have a concrete scenario for how craft could be incorporated into your products, spaces, or client gifts?

How Kogei Japonica Can Help

Kogei Japonica works across overseas communications, corporate procurement introductions, co-creation project coordination, connections to makers and production districts, and on-the-ground reporting and content. Our role is to bridge workshops and businesses with the support organizations and international audiences engaging with Japanese craft.

The most common question we receive is some version of “where do we even start.” If reading this has given you a clearer sense of direction and you need a concrete next step, we are glad to be a starting point for that conversation.

Summary

What METI’s 2026 policy context signals is that the weight placed on sustainability and growth — craft as a functioning industry — is increasing. The sector is being evaluated less on its cultural heritage credentials and more on its capacity to generate value, reach markets, and sustain the people who make it.

The inclusion of Japan’s government-designated traditional craft industries within the creative industries framework in the 12th session materials, and the framing of high-value local creative industries as a growth agenda item, represent a meaningful policy signal for anyone thinking about where traditional craft sits in a longer-term strategy.

Designing sales channels matters more than securing subsidies.

Building ongoing relationships matters more than showing up at events.

Combining craft with other fields to increase value matters more than selling it in isolation.

Creating a revenue structure that makers want to work within matters more than searching for successors.

Policy provides context and, at times, resources. The decisions are made by workshops, organizations, and the businesses that engage with them. The proposals above are not universally applicable prescriptions, but the current policy context does offer a legitimate basis for decision-making — and Kogei Japonica believes that makers who can read that context and use it to inform their own choices will be better placed to sustain craft as a living industry.